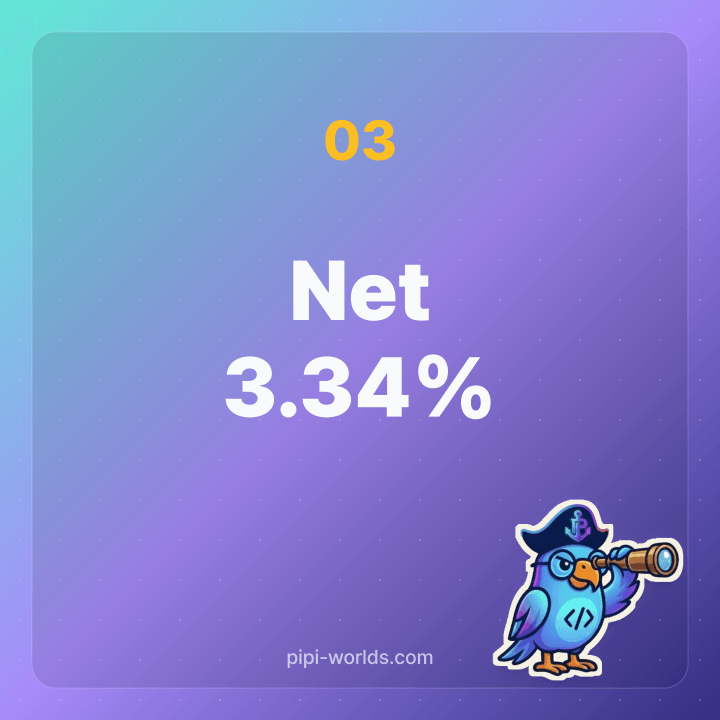

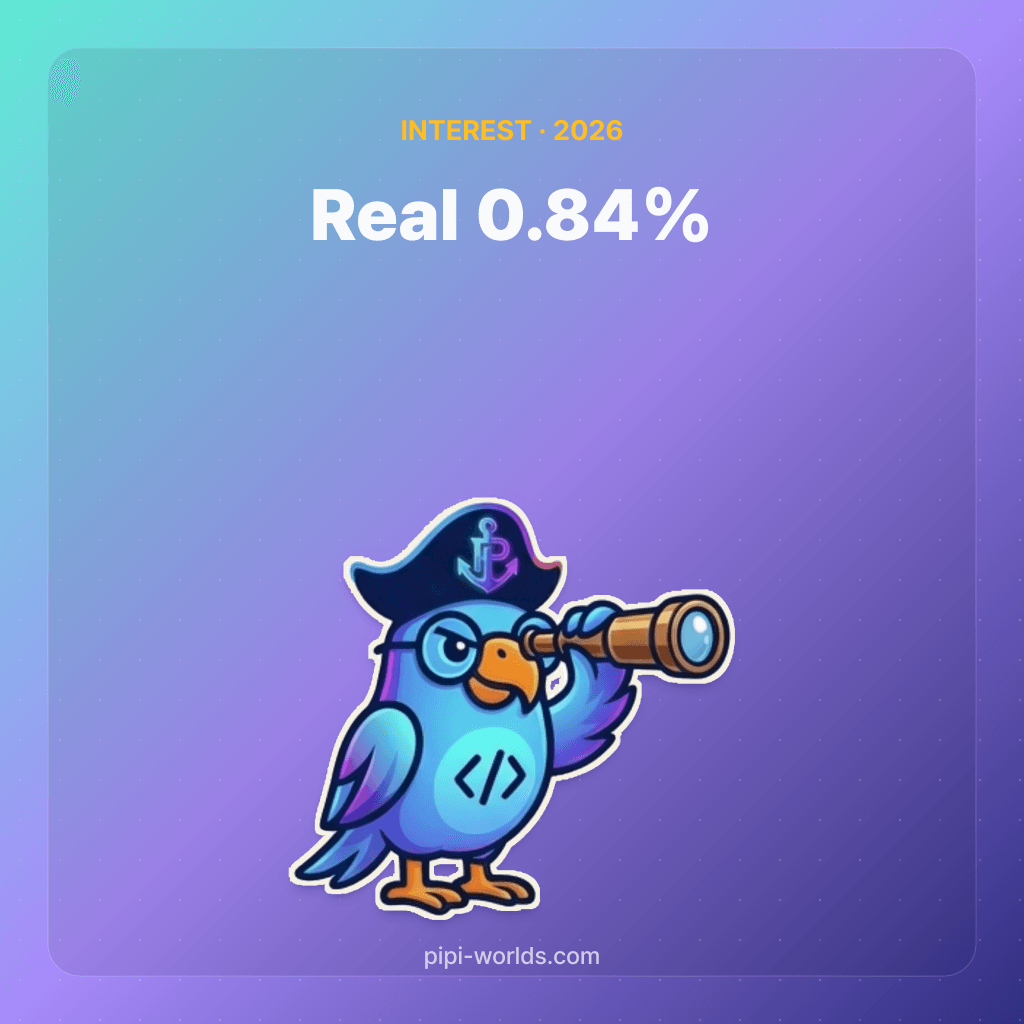

Marcus, Ally, and SoFi all advertise high-yield savings accounts at 5.0% APY. The number sounds great until you do the math: federal income tax (24% for many savers, more in high brackets), state income tax (0-13.3% depending on state), and finally inflation (currently around 2.5%). What started as 5% nominal becomes 3.34% after-tax for a typical California saver, then 0.84% real after inflation. Same dollar amount of cash, vastly different “real” earning power. Understanding nominal vs real return — and the three-step adjustment that gets you from one to the other — is the difference between knowing your money is keeping up with inflation versus quietly losing ground.

$100K, 1 year HYSA — three-step adjustment

For a California saver in the 24% federal bracket and 9.3% state bracket:

| Step | Calculation | Result |

|---|---|---|

| Nominal (advertised APY) | What’s on the bank flyer | 5.00% |

| After-tax | 5.0 × (1 - 0.333 combined) | 3.34% |

| Real (after inflation 2.5%) | 3.34 - 2.5 | 0.84% |

The same 5% APY translates to 0.84% real return for a high-tax-state saver. In Texas (no state tax), the math is better: 5.0 × (1 - 0.24) = 3.80% net, then -2.5% = 1.30% real. Geography shifts the answer significantly.

The interest tool lets you toggle “Tax on” and enter your federal and state marginal rates to see the after-tax number directly. Then mentally subtract 2.5% to get real.

Why 2.5% inflation is the working assumption

The actual U.S. inflation rate fluctuates. Recent values:

- 2024 CPI: 2.9% (Bureau of Labor Statistics)

- 2025 CPI through October: 2.6%

- Federal Reserve target: 2.0%

- 2026 FOMC projections (median): 2.3-2.5%

The 2.5% in this article is a midpoint of recent actual rates and Fed projections. It will fluctuate with energy prices, supply chains, and Fed policy.

Negative real rates hurt slowly but devastatingly

The same $100K parked in a checking account at 0.01% with 2.5% inflation:

| Time horizon | Nominal balance | Purchasing power |

|---|---|---|

| Year 0 | $100,000 | $100,000 |

| Year 1 | $100,010 | $97,571 |

| Year 5 | $100,050 | $88,386 |

| Year 10 | $100,100 | $78,121 |

| Year 20 | $100,200 | $61,029 |

| Year 30 | $100,300 | $47,674 |

Over 30 years, “safe” checking account preserves the nominal $100K but loses $52,000 in real purchasing power. The illusion of safety hides the reality of slow decay.

Inflation-resistant assets ranked by real return

| Asset | Nominal long-term avg | Real return (after 2.5% inflation) |

|---|---|---|

| Checking account | 0.01% | -2.5% |

| HYSA at peak | 4-5% | +1.3% to +2.3% (TX) / +0.5% to +1.0% (CA) |

| 1-Year Treasury Bills | 4.5% | +1.55% (state-tax exempt) |

| TIPS (10-year) | CPI + 1.5% real | +1.5% (locked) |

| S&P 500 index | 10% nominal historic | +7.5% real |

| Real estate (residential) | 4-6% nominal | +1.5% to +3.5% |

| Series I Bonds | CPI-linked | ~CPI rate |

Equities provide the strongest long-term inflation hedge. TIPS and I Bonds give explicit inflation protection at lower (but locked) rates. Real estate combines inflation tracking with rental yield. Most diversified portfolios use multiple of these.

Tax-advantaged accounts amplify real returns

Same equity index in different wrappers:

| Wrapper | Nominal | After-tax | Real (-2.5%) |

|---|---|---|---|

| Taxable account | 10% | 6% (15-20% LTCG) | +3.5% |

| Roth IRA | 10% | 10% (tax-free) | +7.5% |

| 401(k) Traditional | 10% | 10% growth + ord. income later | ~+5% effective |

| HSA (qualified medical) | 10% | 10% (triple tax-free) | +7.5% |

Roth IRA and HSA produce the best real returns because growth is genuinely tax-free at withdrawal. 401(k) Traditional has the largest annual contribution limit ($23,500) but withdrawals are taxed. The combination of equities + tax-advantaged wrappers + low-cost index funds is the standard recipe for beating inflation over decades.

How to model real returns in the interest tool

The interest tool doesn’t directly subtract inflation, but you can model it by:

- Enter the nominal rate and turn on the “Tax on” toggle with your federal + state rates.

- Read the after-tax effective rate from the result.

- Mentally subtract your assumed inflation rate (2.5% standard).

- The remainder is your real return.

For comparing investment vs savings, build two scenarios in the compare panel: HYSA at 5% nominal vs S&P 500 (10% nominal) over 10 years. The compounded difference in nominal terms makes the case visually, and you can apply the inflation discount equally to both.

Key takeaways

- Nominal rate is marketing. Real rate is what you can spend.

- Tax wrappers matter more than rate spreads. A Roth IRA + index fund beats a 6% taxable account easily over 30 years.

- Don’t park long-term money in low-yield “safe” accounts. Negative real returns compound destructively over decades.

- Mix inflation hedges. Equities for long-term, TIPS/I Bonds for explicit protection, HYSA for emergency only.

- 2.5% is a working assumption. Real inflation will be 1.5-3.5% in most years. Build a margin of safety.

A $100,000 sitting in a low-interest savings account isn’t preserved wealth — it’s slowly evaporating purchasing power. The simplest defense is moving most of that capital into vehicles that at minimum match inflation (TIPS, I Bonds) and ideally beat it (equities, real estate). The interest tool helps you see the difference one decision at a time, but the real lesson is structural: build your portfolio around real returns, not nominal yields. The bank statement will look the same; your future buying power will be entirely different.